The Retirement Risk No One is Planning For

How Cyber Fraud Threatens Retirement Savings and Demands Immediate Action

Quarter Mile Q2 2026

For most Canadians, retirement planning revolves around a familiar set of concerns: saving enough via Canada’s three-letter and four-letter system (RRSPs, FHSAs, TFSAs, IPPs, CPP, OAS) and then figuring out how to manage core risks like market swings, inflation, health-care costs, emotions, longevity, and taxes.

These well-known accumulation and decumulation challenges have received deserved attention from academics, wealth professionals, and DIY investors.

But with the rise of online banking and artificial intelligence, something has significantly changed.

Almost everything financial runs through digital channels, and the tools we use to build and manage retirement wealth have evolved. Banking, bill payments, RRSP contributions, pension transfers, tax filings, and government benefits are all happening online.

A lifetime of savings is now reachable through devices that can be compromised by anyone, anywhere in the world. Financial planning has yet to catch up.

In this paper, we document:

1. The Scale of the Modern Fraud Problem

2. Why Individual Fraud Losses are a Retirement Risk

3. How Losses to Fraud Create a Permanent Loss of Capital

4. Nine Strategies to Protect Ourselves from Digital Risks

We aim to make the case that cyber fraud is now a permanent feature of the financial landscape, and thus a permanent “tail risk” to retirees. Our thesis is that cyber and fraud risks deserve to be included in every financial plan’s addressable retirement risks alongside investment markets, inflation, sequence of returns, longevity, and taxes.

1. The Scale of the Problem

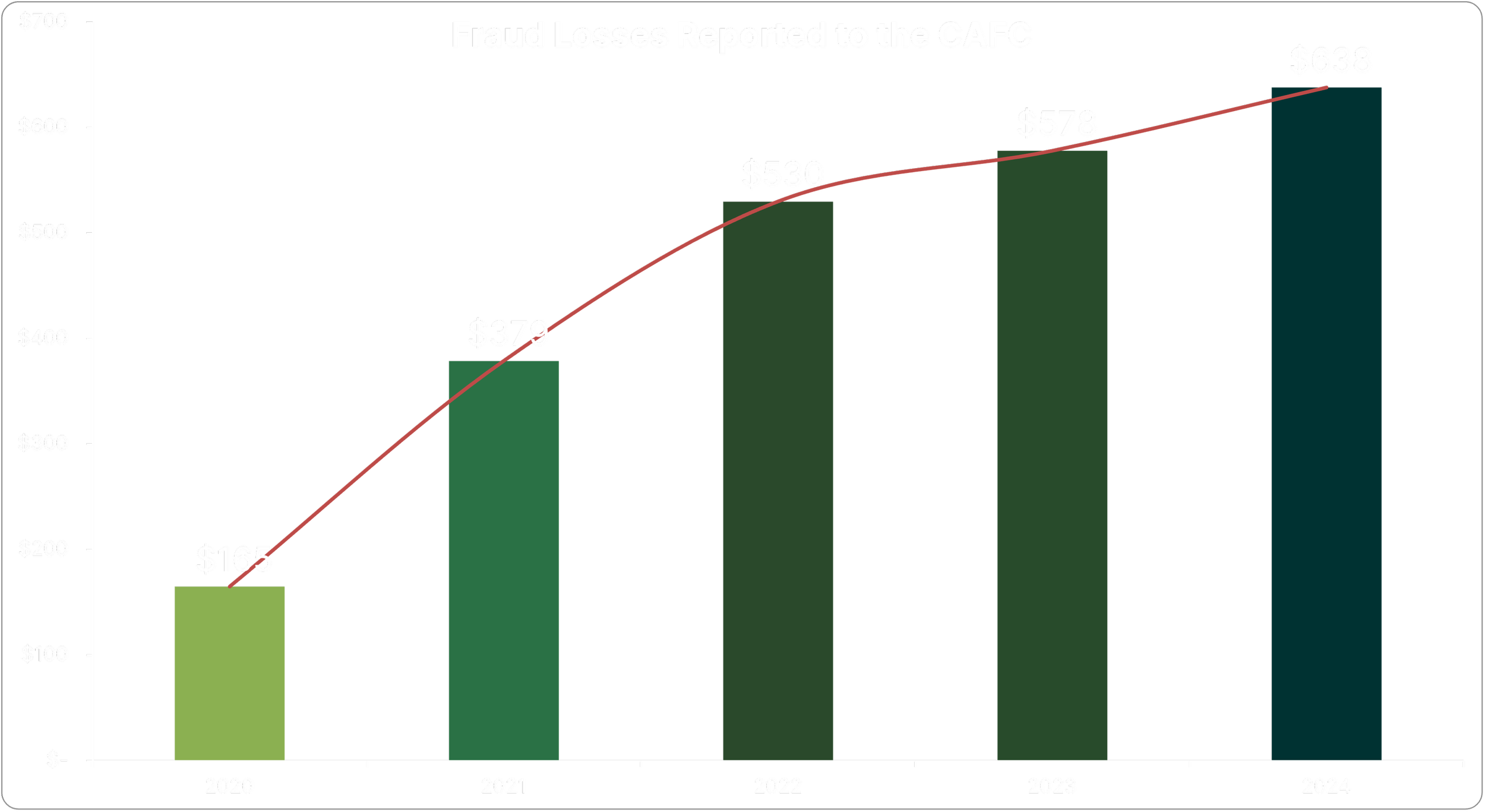

Canada’s fraud numbers tell a stark story. Losses reported to the Canadian Anti-Fraud Centre (CAFC) have climbed sharply (Chart 1). Modern digital technologies are compounding these dramatic increases, enabling criminals to use AI-generated voice clones, deepfake videos, and phishing emails that are progressively harder to differentiate from the real thing. Most disturbingly, this is not a temporary spike; it is a permanent shift in the risk landscape.

Chart 1: Canadian Fraud Loss Increases 2020 – 2024 1,2,3

Under the Surface, Even Worse

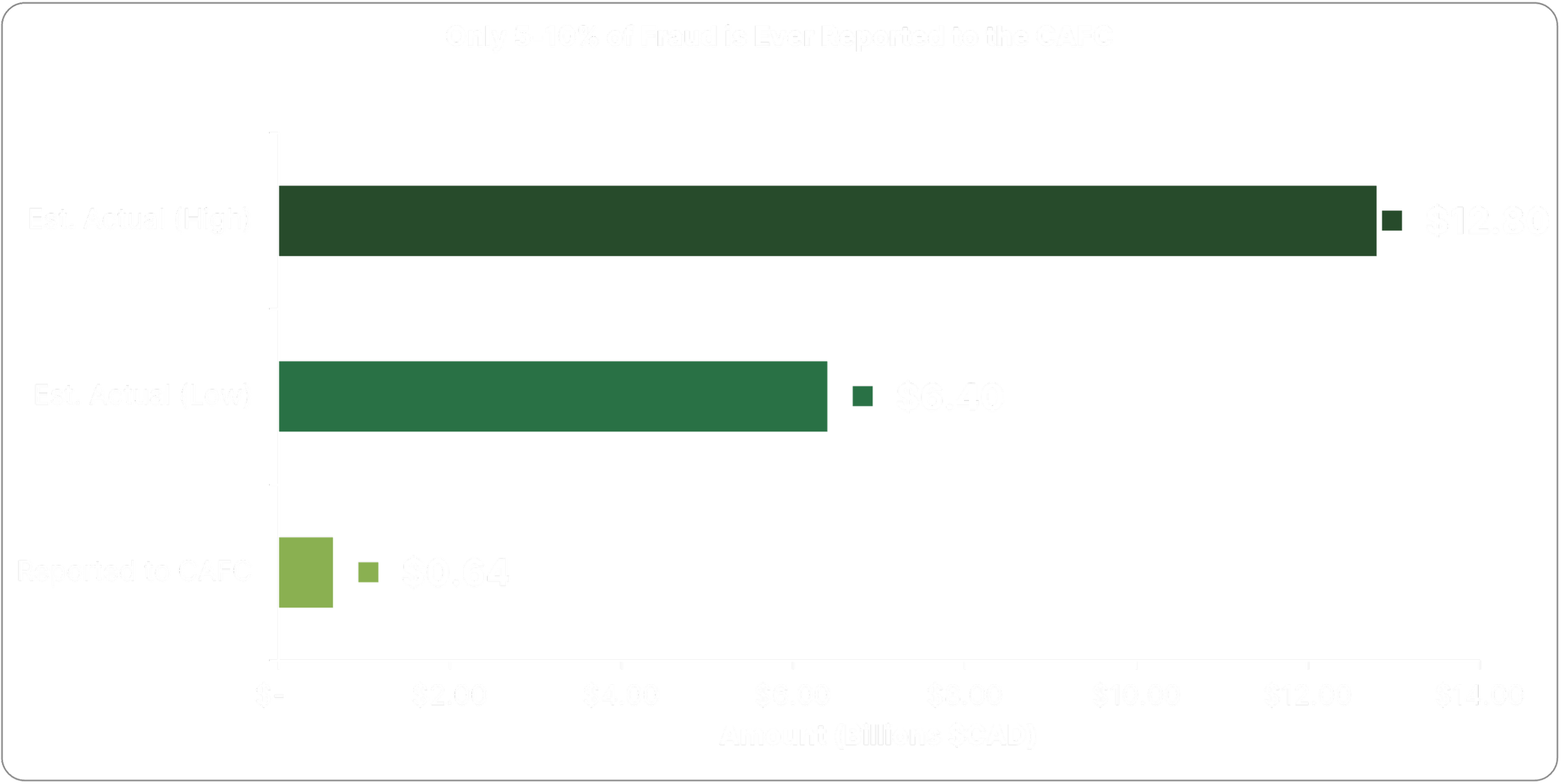

Unfortunately, researchers advise that this data is probably considerably understated. Fraud and loss carry a great deal of emotional trauma, including shame and self-blame, and most victims never come forward to report their experiences. McMaster University and Statistics Canada research puts the fraud reporting rate at just 5% to 10%, meaning that the level of reported loss should be increased by 10x to 20x (Chart 2).

Chart 2: Fraud Losses Adjusted for Underreporting (2024) 1,4,5

While $12.8 billion in fraud losses is an enormous tragedy, it is relatively small at just 0.07% of Canada’s total household net worth of $17.5 trillion. It is our belief, however, that the impact on a small group of individuals is dramatically more damaging than this number lets on.

2. What an Individual Loss Actually Looks Like

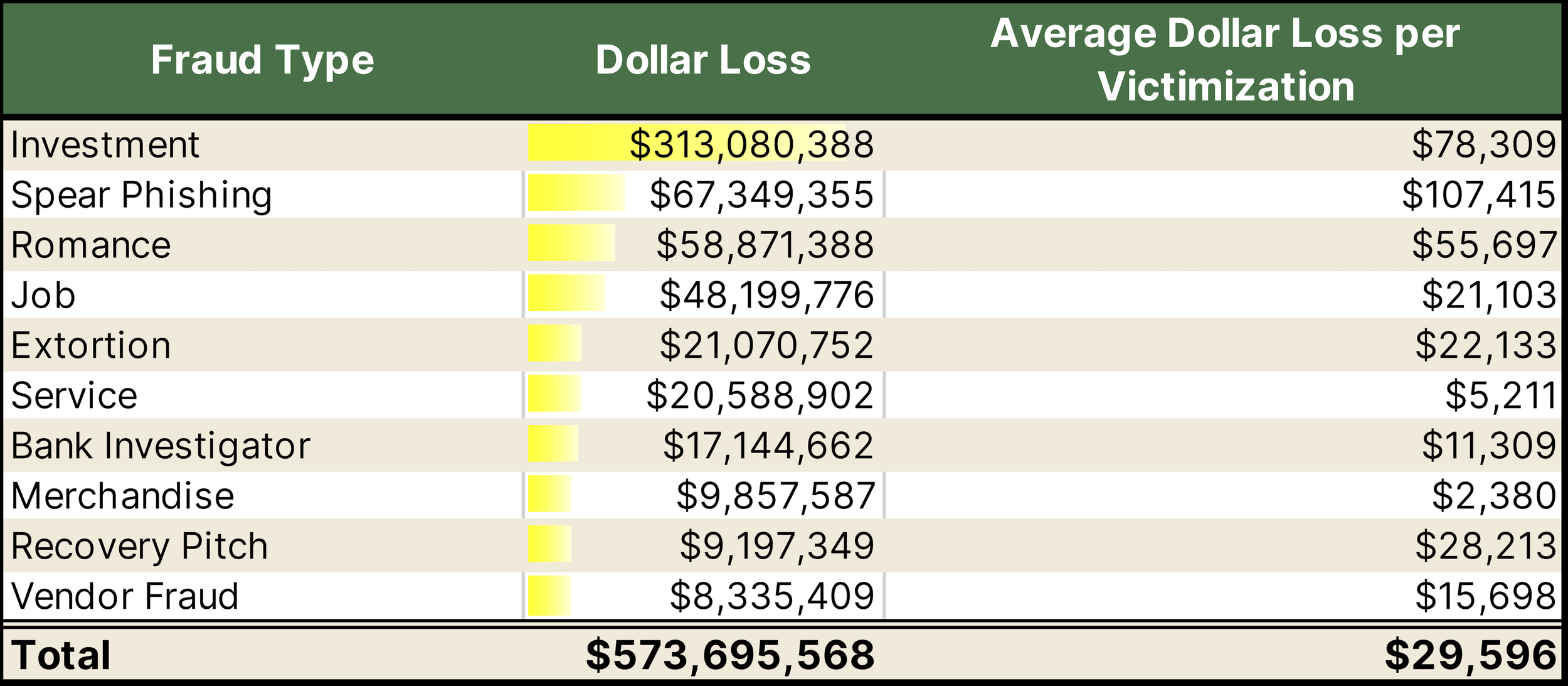

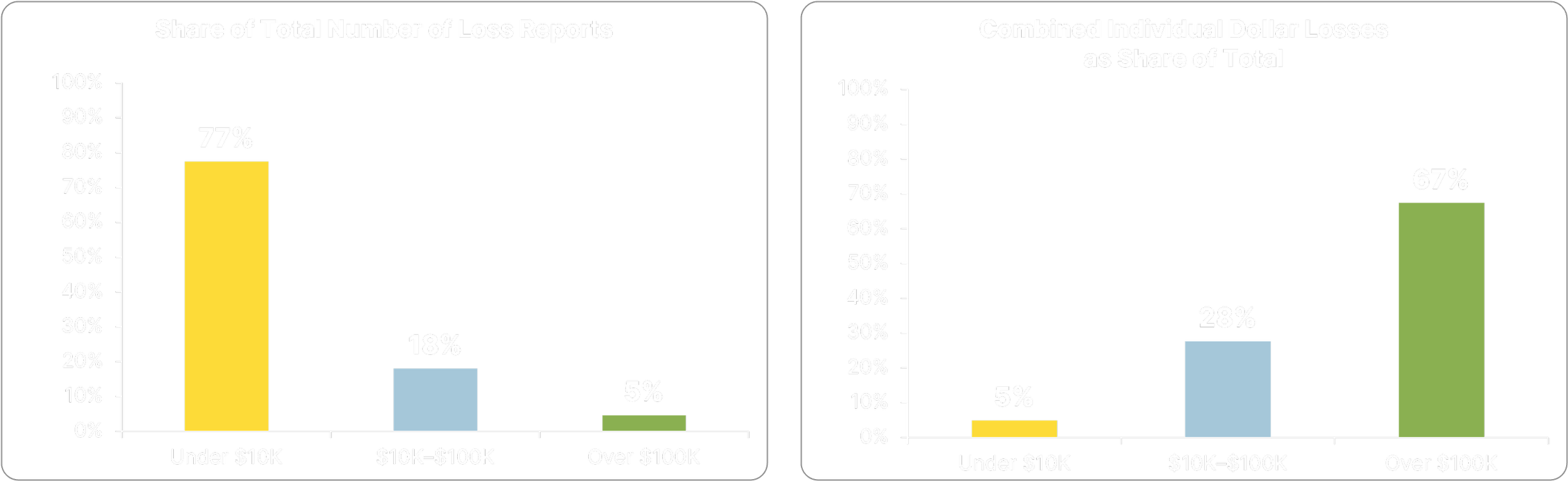

While aggregate fraud losses are shocking, the impact on individuals hit by rare yet extreme loss scenarios is devastating. When an unlikely but large loss occurs in stock markets, investment managers often refer to this as a ‘tail risk.’ We posit that the three largest “loss per victimization” categories – investment fraud, spear phishing, and romance scams (Chart 3) – deserve to be classified as retirement tail risks.

Chart 3: Frauds with the Largest Dollar Losses1

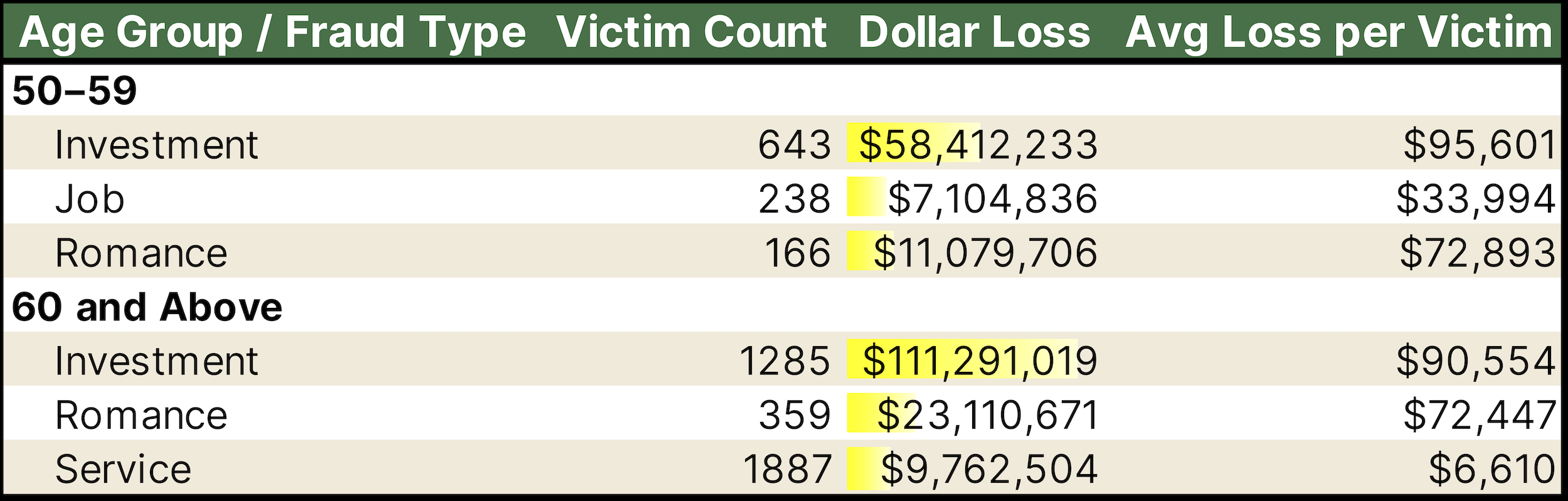

While most seniors will not experience a loss in any given year, when tail-risk fraud hits individuals approaching or in retirement, it is larger than average, concentrated, and catastrophic (Chart 4). This is particularly true considering that the average value of liquid investment assets (referred to by Statistics Canada as “other financial assets”) is $592,076 for Generation X and $694,678 for Baby Boomers.6

A fraud loss of $90,000, then, means a loss of 12% to 15% of spendable assets on average.

These tail-risk events are what make cyber fraud so dangerous: rare enough to ignore, severe enough to permanently harm retirement.

Chart 4: Large Dollar Fraud Losses are Retirement Tail Risks1

Not Just a Canada Problem: Data from the United States

Fraud and loss data in the United States supports our thesis. Data from the Federal Trade Commission (FTC) report “Protecting Older Consumers 2024 – 2025” lists the median loss experienced by people over 60 at $900, a troubling but potentially manageable amount. Once again, however, this hides the devastating tail risk hiding under the surface: according to the FTC, 5% of reports from older adults were for losses greater than USD$100,000. 7

Chart 5: U.S. Reported Losses Confirm Retirement Tail Risk (Older Adults 60+, 2024) 8

While U.S. liquid assets data is calculated differently than in Canada, we can estimate a similar metric for U.S. spendable assets. Based on the U.S. Survey of Consumer Finances (2022), the average value of financial assets (excluding real estate, vehicles and non-stock business equity) for Generation X and Baby Boomers is between USD$430,000 and USD$896,000. 9

Based on this data, for individuals in or approaching retirement in the United States, fraud loss of $100,000 means a loss of between 11% and 23% of spendable assets, on average.

Unfortunately, the FTC report also advises that this risk is increasing:

“From 2020 to 2024, combined losses by older adults who reported losing over $100,000 increased more than fivefold … Controlling for population size, older adults were nearly twice as likely as younger adults to report a six-figure fraud loss.”7

3. Why the Money Almost Never Comes Back

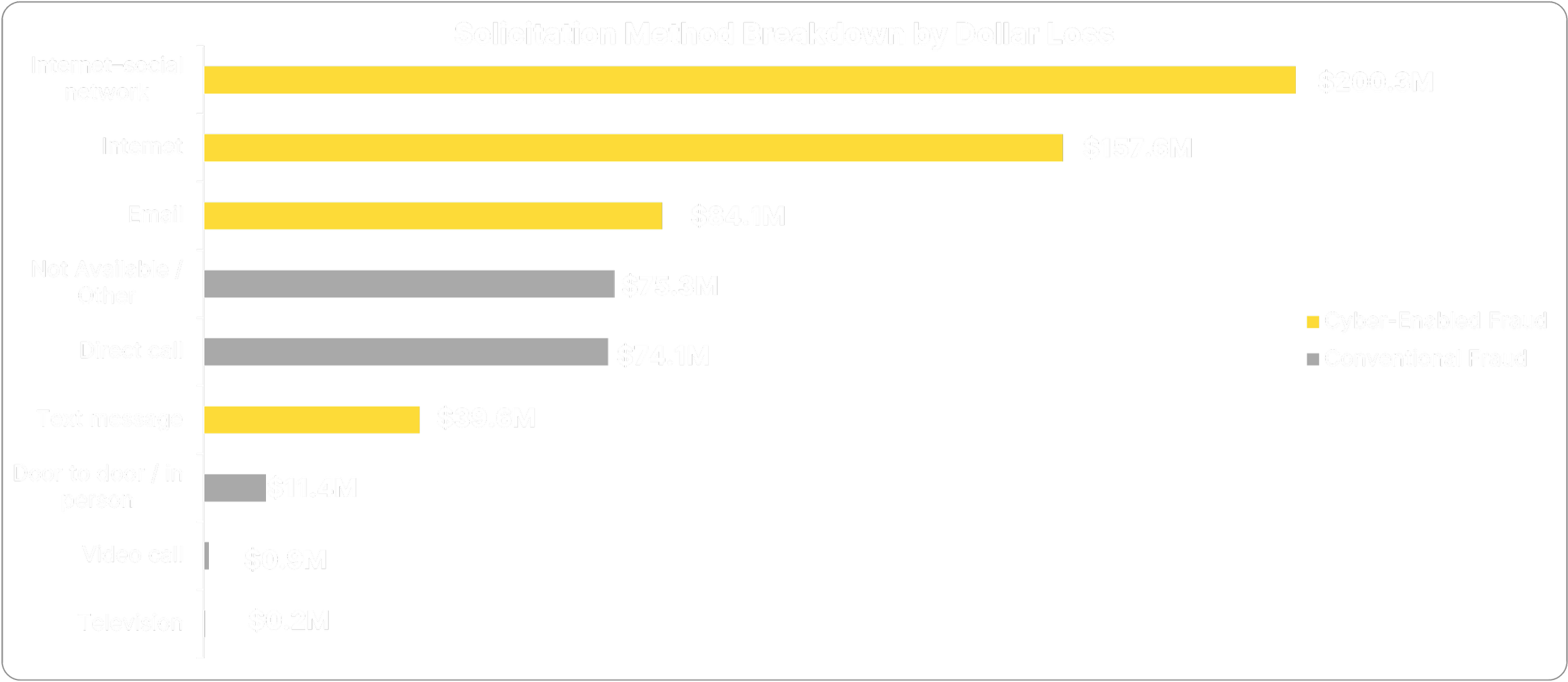

Across Canada and the United States, cyber-connected fraud is leading to the worst outcomes for victims. With the ubiquity of online life, this challenge is accelerating; cyber is the leading solicitation method for fraud, when measured by dollars lost.

Chart 6: Cyber-Enabled Fraud Leads to Larger Losses 1

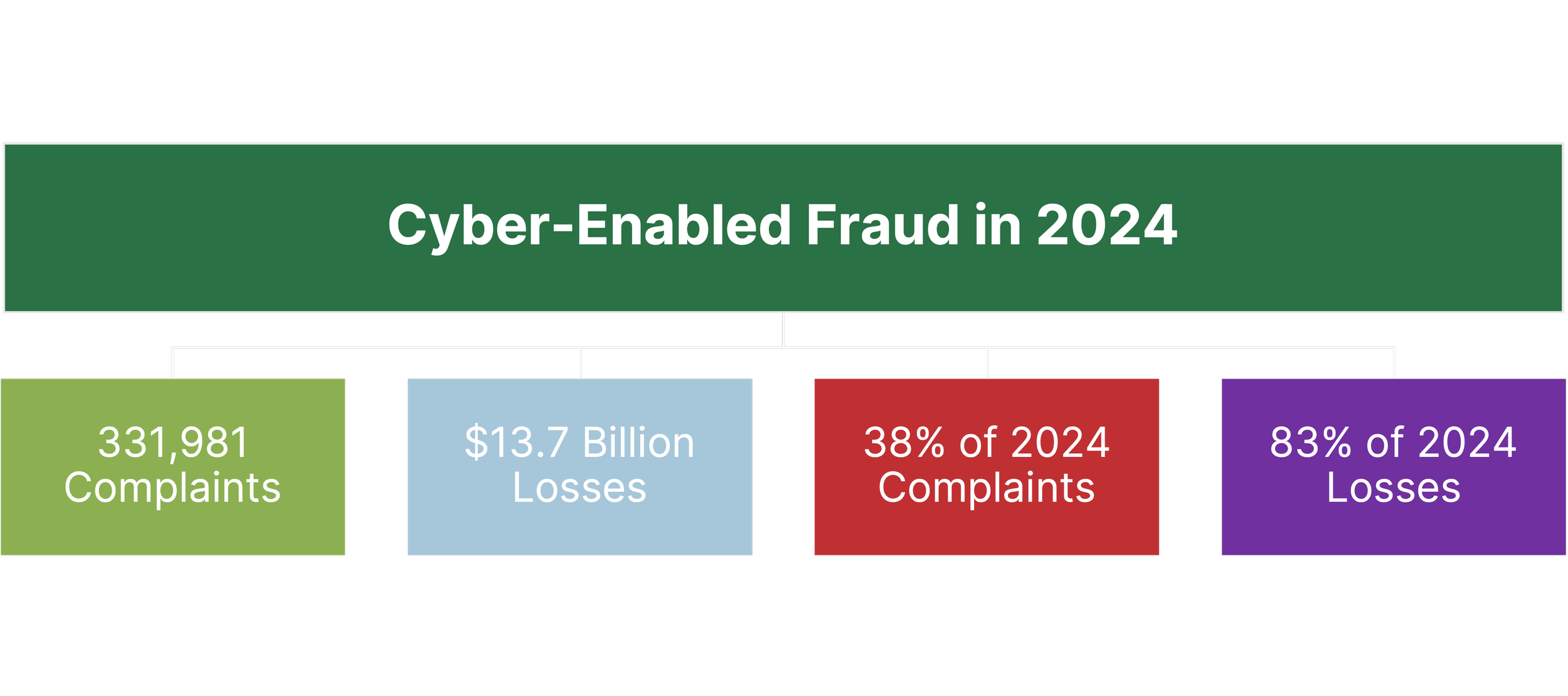

This is not unique to Canada. In the U.S., cyber-enabled fraud was responsible for almost 83% of all losses reported to the FBI in 2024. 10

Chart 7: U.S. Statistics for Cyber-Enabled Fraud (2024) 10

Methods of Loss

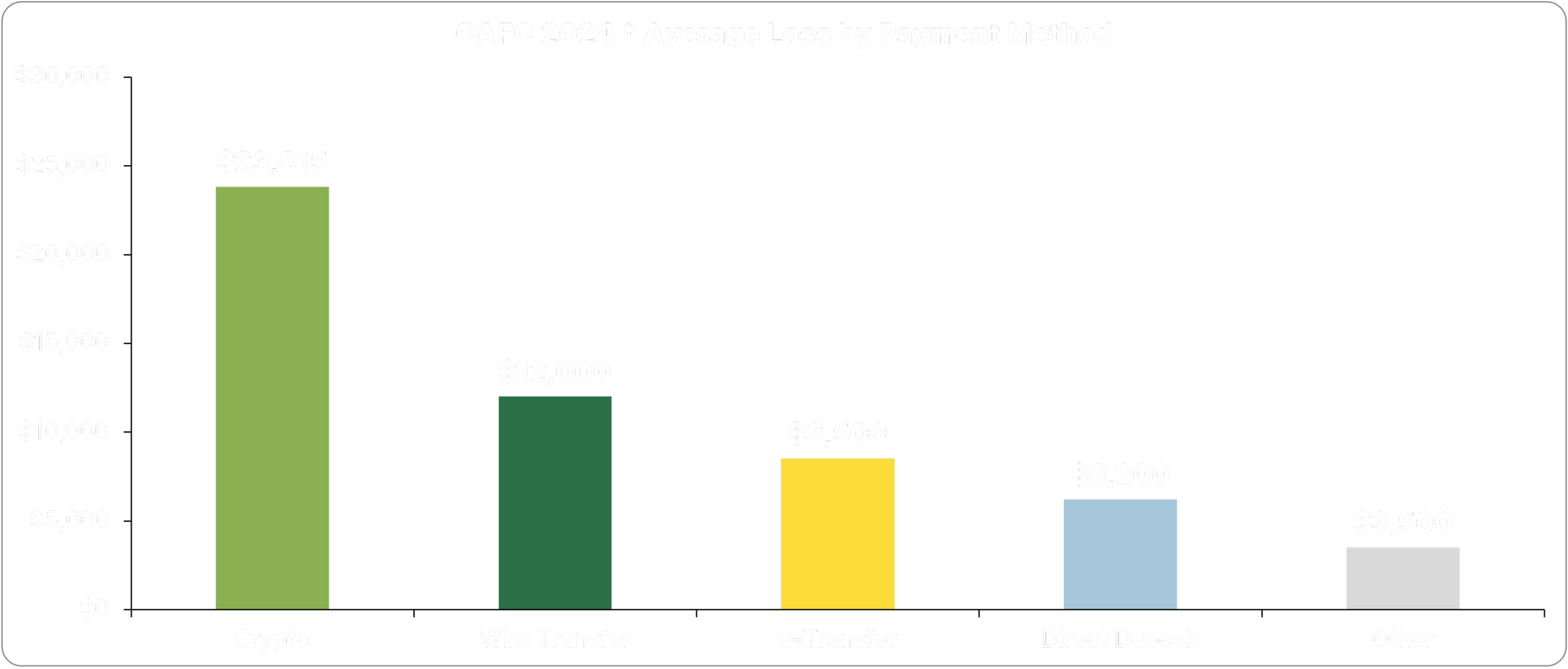

Cyber-enabled money transfer technologies also contribute to larger individual losses.

Cryptocurrency is gone. Once converted and transferred, cryptocurrencies can be functionally unrecoverable. While some exceptionally large frauds have reportedly been recovered by law enforcement, smaller amounts are unlikely to receive attention and resources. Crypto fraud in Canada averaged $23,815 per transaction in 2024.1

Wire transfers are hard to reverse. Banks may not claw back authorized transfers, even if you were deceived11,12.

e-Transfers are growing fast. Losses through e-transfers grew 26.1% in 2024 in Canada.1

Insurance may not cover it. Home and umbrella policies can exclude “voluntary transfers” — which is how financial institutions may classify transfers made under a scammer’s influence13.

Chart 8: Cryptocurrency Carries the Highest Average Loss

4. Protecting Ourselves

While in this paper we use investment terminology like “tail risk” to highlight the rare but dangerous nature of cyber fraud, it is important to be clear about the biggest difference between fraud risk and market risk.

If a market portfolio drops by 30%, for example, history has shown that portfolio can recover.14 If a fraudster steals $100,000, though, that money is likely to be a permanent loss of capital and a permanent reduction in standard of living.

Long-term investors diversify portfolios against market crashes. They plan for inflation, longevity, even health-care costs. We even insure our homes against fire. But, what about a risk that is more permanent than a market crash? The current approach to managing this risk is for institutions to provide warning emails and pop-up screens. Few, if any, retirement plans prepare seniors for the risk of cyber fraud.

Retirees must take digital security into their own hands.

Financial planners should start building cyber risk into retirement plans.

Here are our immediate recommendations, based on the most prevalent forms of fraud (including identity theft), as well as forms of fraud with the highest dollar losses like investment fraud, spear phishing, and romance scams:

1. Identity Theft and Fraud:

Get to know the credit agencies: It is easier and easier to stay on top of your credit score and any transactions happening on your credit profile. The credit agencies, Equifax and TransUnion, will provide a copy of your credit report but we recommend a subscription to a monitoring service. A monitoring service will provide real time credit monitoring alerts so you can watch for fraudulent activity, as well as other services like dark web and social media monitoring.

Credit Lock or Credit Freeze: While freezing one’s credit is relatively simple in the United States, this is an area of provincial jurisdiction in Canada; so far, this is only available in Quebec.

2. Investment Fraud:

- Know the tactics: Investment fraud often follows a compelling, emotion-triggering pattern. Watch for urgency, exclusivity, and abnormally high returns. If you are having an emotional reaction (excitement, greed, fear, or a need to move fast), slow down and be very careful.

- Understand if you fit the profile: Some research is showing victims of investment fraud are more likely to have a specific demographic profile: Higher non-housing wealth, male, older, and are more likely to buy investments “sold through unsolicited calls, emails, ads, or ‘free lunch’ seminars.”15,16 If you (or your clients) fit this profile, know thyself and be warned.

- Check the registration: In both Canada and the United States, firms and advisors should be registered. In Canada, clients can check the National Registration Search. In the U.S., clients can check FINRA’s BrokerCheck.

3. Spear Phishing and Romance Scams:

Beware social media and your personal details: Social media disclosures are jet fuel for trust-based swindles like spear phishing and romance scams.

Spear phishing is a targeted fraud attempt based on information that is specific to you. For example, you complain about your bank on Facebook, and then get an email from your bank promising resolution if you click on the link in the email.

Romance frauds (also known as relationship frauds when connected to family, friends or professional contacts) involve the building of trust and affection over prolonged periods of time to gain access to financial accounts and assets.

4. All Fraud Types:

- Assess your personal risk: Taking a robust assessment to determine risk areas and steps for mitigation is an absolute necessity. Retirees with no technology support via a workplace are often unaware of the different vectors of attack in their digital, social media, and financial lives. As we feel this type of assessment is so important, our website includes an abridged version of our risk assessment questionnaire that can be done by anyone for free: Digital Risk Advisory | Enhance Digital Security Now — North Road Investment Counsel

- Trusted contact or second opinion contact: Financial advisors should be maintaining for every client a “trusted contact”, a person the client designates as a connection who can be contacted if the advisor has concerns about the client. It is also worth documenting (either with your advisor, or on one’s own) someone who has the skills to provide a ‘sober second thought’ on investment opportunities.

- Hopefully clients view financial planners and investment counsellors as a sounding board for any outside opportunities, but helping the client think of a trusted friend with financial wherewithal prior to an investment fraud encounter could be a best practice for any advisory team.

- Monthly Awareness: Research shows that fraud awareness and detection training improves our ability to recognize swindles; however, the beneficial effect declines within weeks17,18. We recommend subscribing to fraud or scam awareness newsletters with a frequency of at least monthly.

- Update your password hygiene: Password manager apps with military grade encryption are available and are well worth the small subscription cost.

- In addition, always use multi-factor authentication on websites, if available.

While this is not an exhaustive list, we feel these recommendations start retirees and their financial advisors in the right direction. The data is clear: cyber fraud is a major tail risk facing all retirees and the greater one’s wealth, the greater the risk of large losses. It is incumbent upon the investment management industry to get beyond email warnings and find fulsome ways to help clients button up their digital risk.

Sources

[1] “2024 Annual Statistical Report”. Canadian Anti-Fraud Centre. (2025) https://open.canada.ca/data/en/info/69c68f22-8a2a-43d1-8f4e-4017e3ffebba

[2] “2022 Canadian Anti-Fraud Centre’s Annual Report 2022”. Canadian Anti-Fraud Centre. (Updated 2024) https://open.canada.ca/data/en/info/69c68f22-8a2a-43d1-8f4e-4017e3ffebba

[3] “2021 Canadian Anti-Fraud Centre’s Annual Report”. Canadian Anti-Fraud Centre. (Updated 2024) https://open.canada.ca/data/en/info/69c68f22-8a2a-43d1-8f4e-4017e3ffebba

[4] The Cost of Fraud Exceeds Financial Loss”. RCMP Gazette. (2025). The cost of fraud exceeds financial loss, victims say | Royal Canadian Mounted Police

[5] “Self-reported fraud in Canada, 2019”. Government of Canada. (2023) Self-reported fraud in Canada, 2019

[6] “Canadians’ average wealth hit $1.07 million, but what’s driving net worth depends on your age, province and bracket.” Financial Post. March 13, 2026. Canadians’ average household wealth hit $1.07 million in Q3 | Financial Post

[7] “Protecting Older Consumers 2024–2025 A Report of the Federal Trade Commission”. U.S. Federal Trade Commission. December 1, 2025. Protecting Older Consumers 2024-2025 (A Report of the Federal Trade Commission)

[8] Chart 5: U.S. Reported Losses Confirm Retirement Tail Risk. Developed with Microsoft Copilot using data from Protecting Older Consumers 2024-2025 (A Report of the Federal Trade Commission).

[9] “Financial assets by age of reference person, Mean ($)”. Survey of Consumer Finances, 1989 - 2022. Board of Governors of the Federal Reserve System. The Fed - Table: Survey of Consumer Finances, 1989 - 2022

[10] “Federal Bureau of Investigation Internet Crime Report 2024”. FBI Internet Complaint Centre. https://www.ic3.gov/AnnualReport/Reports/2024_IC3Report.pdf

[11] “Bank denies liability after alleged $343K misdirected deposit”. CTV News. https://www.ctvnews.ca/winnipeg/article/bank-denies-liability-after-alleged-343k-deposited-into-wrong-account-funds-withdrawn/

[12] “Winnipeg woman slams bank's decision not to refund her after 'dumbfounding' scam”. CBC News. https://www.cbc.ca/news/canada/manitoba/winnipeg-scam-td-bank-fraud-appeal-denied-9.7154235

[13] “Consumer Bulletin: Understanding Fraud Protection”. Ombudsman for Banking Services and Investments (OBSI). https://www.obsi.ca/en/news/posts/consumer-bulletin-understanding-fraud-protection/

[14] What We’ve Learned From 150 Years of Stock Market Crashes”. Morningstar. https://www.morningstar.com/economy/what-weve-learned-150-years-stock-market-crashes

[15] Deliema, M., Shadel, D., & Pak, K. (2020). Profiling Victims of Investment Fraud: Mindsets and Risky Behaviors. Journal of Consumer Research, 46(5), 904-914. https://doi.org/10.1093/jcr/ucz020

[16] Deliema, M., Deevy, M., Lusardi, A., & Mitchell, O. S. (2020). Financial fraud among older americans: Evidence and implications. Journals of Gerontology - Series B Psychological Sciences and Social Sciences, 75(4), 861 868. https://doi.org/10.1093/geronb/gby151

[17] DeLiema, M., Robb, C. A., & Wendel, S. (2025). What does trust have to do with it? Training consumers to detect digital imposter scams. Journal of Financial Crime, 32(1), 77-97. https://doi.org/10.1108/JFC-12-2023-0314

[18] DeLiema, M., Li, Y., & Mottola, G. (2023). Correlates of responding to and becoming victimized by fraud: Examining risk factors by scam type. International Journal of Consumer Studies, 47(3), 1042-1059. https://doi.org/10.1111/ijcs.12886

Disclaimer

This document is provided for informational purposes only and does not constitute investment, financial, legal, or cybersecurity advice. In our opinion, the information presented reflects common practices, general observations, and academic research; however, it may not be appropriate for all individuals or situations. The content is intended to support general understanding and awareness and should not be relied upon as a substitute for professional advice.

While we strive to offer effective guidance on digital safety, we cannot guarantee absolute protection against all online threats. The rapidly evolving nature of digital risks means that no measures can ensure complete security. As a result, it is not possible to provide guarantees of safety in connection with our Digital Risk Program. Any information or guidance given to address specific issues are based on best efforts and should not be construed to guarantee protection or to exhaustively address such issues.

Please note that any recommendations we provide are entirely optional, and you are under no obligation to act upon them. Should you choose to implement our suggestions, we may recommend you engage third-party service providers to implement some, or all, of the recommendations developed as part of Digital Risk Program. We do not receive compensation for referring these third-party providers, nor are you required to work with any third-party we recommend. Any engagement with a third-party provider is solely between you and the third-party. We recommend you perform your own due diligence on the expertise of third-party providers recommended by North Road. Any action taken by you or a third-party provider based on information, suggestions, or guidance provided by North Road under the Digital Risk Program is entirely the responsibility of the acting party and North Road does not take any responsibility or ownership of any such action.

All opinions, projections and estimates herein reflect the author's judgment as of the date of the document, may not be realized, and are subject to change without notice. Nothing in this document is or should be relied upon as a promise or representation as to the future.

©2026 North Road Investment Counsel Inc. All rights reserved.