SpaceX IPO or: How I Learned to Stop Worrying and Love Elon

Should long-term investors participate in Initial Public Offerings (IPOs)?

Quarter Mile Q3 2026

“Gentlemen, you can't fight in here! This is the War Room.”

- President Merkin Muffley, “Dr. Strangelove or: How I Learned to Stop Worrying and Love the Bomb”

The headlines almost write themselves: The largest IPO in history. An expected $1.77 trillion valuation. Likely among the top ten most valuable U.S. companies on its first day of trading on public markets. SpaceX (SPCX) is generating enough noise pre-IPO (Initial Public Offering) that it is almost inescapable for investors and market followers. But headlines never explain the most important questions behind a complex story:

• What am I actually buying?

• What risk am I accepting?

• How does this align with my goals?

What Are We Buying

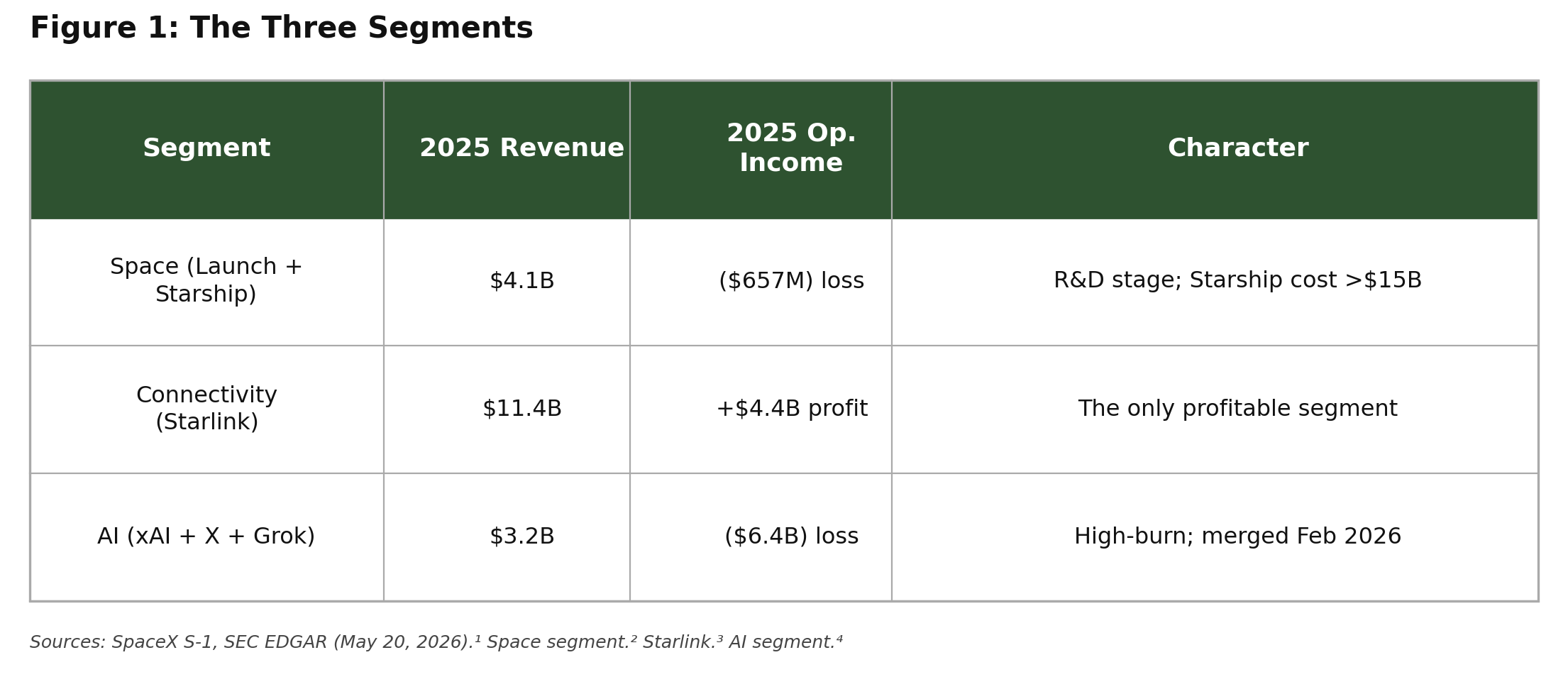

SpaceX as it appears in the S-1 filing¹ is not the company many investors imagine from headlines. It encompasses three materially different businesses consolidated under common-control accounting, meaning the financials have been retroactively combined as though they were always one entity. Perhaps more importantly, despite billions in revenue, the full entity is not yet profitable. Figure 1 shows a quick summary of the business units and key details. (Note: All figures in this white paper are USD)

Figure 1: The Three Segments

Key Insight

Investors are not being asked to buy a “spaceship company” (i.e. Starship). They are not even being asked to buy a satellite company (i.e. Starlink). We are being asked to buy a profitable satellite company, plus an early-stage and unprofitable rocket program, plus an artificial intelligence and social media company burning more cash than the profits of all divisions combined.

What Price are We Paying

With the SpaceX IPO priced at $135 per share⁵, the implied valuation for the firm is about $1.77 trillion dollars. The beauty of public markets (unlike private markets) is that investors get full transparency into the business and the resulting valuation metrics.

Valuation multiples are instructive. While not a hard and fast rule, in general, high valuations today are expected to produce low returns in the future for investors.

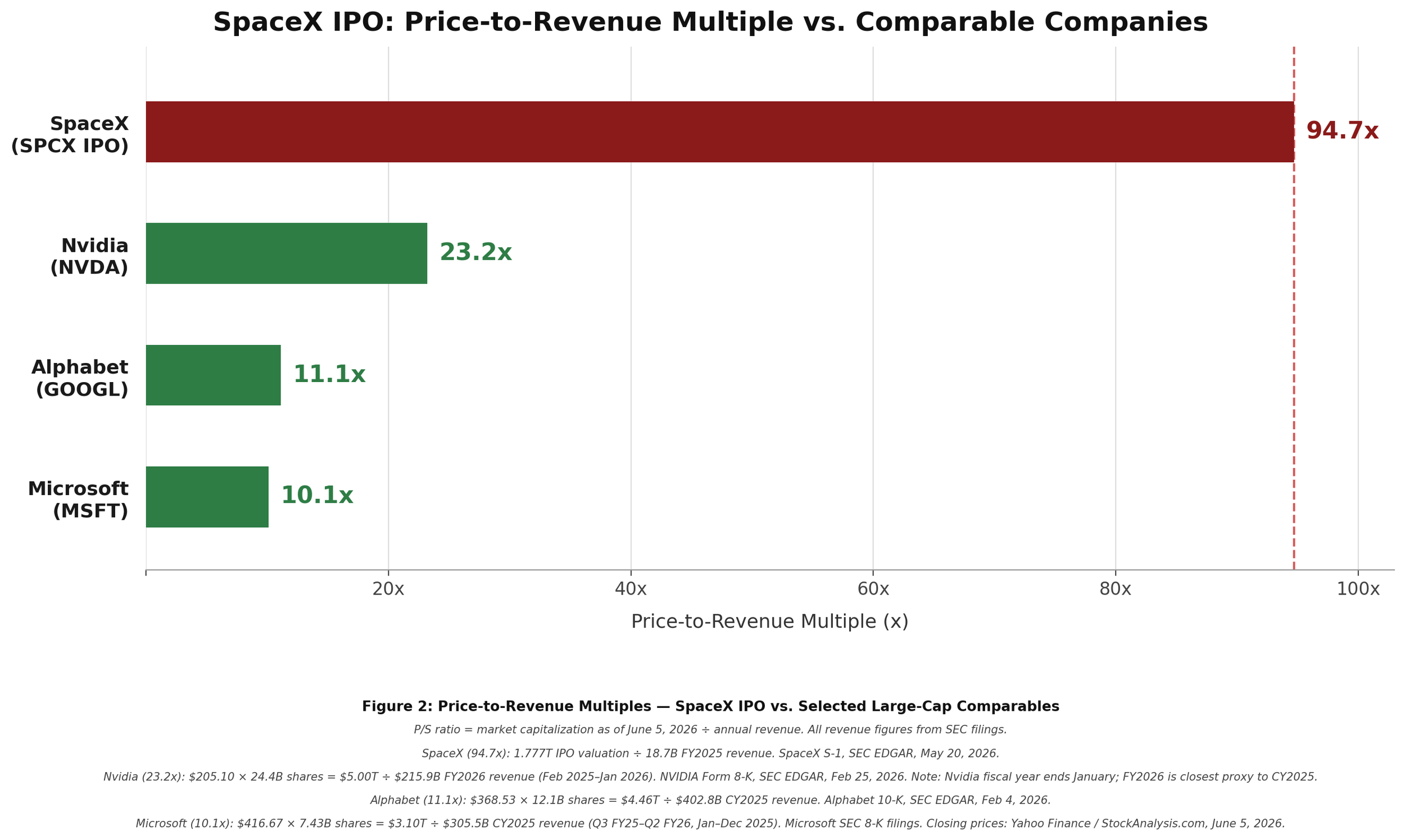

SpaceX is expected to be priced at about 94 times revenue. Not 94 times profits, (profits are negative after all), but 94x last year’s sales.

When reviewing companies valued in trillions of dollars and valuations in the double digits, it can be challenging to grasp the scale of this data. One way to feel the scale of 94 times revenue is by comparing to other companies.

Alphabet/Google, for example, generated $402.8 billion in revenue in 2025.⁶ If we apply a 94x multiple to Alphabet’s sales, it would imply a valuation of roughly $37.9 trillion for Alphabet, more than half of the entire current market capitalization of the US stock market. Figure 2 below compares SpaceX revenue multiples to other tech companies and tech-focused markets.

Figure 2: Comparable Revenue Multiples¹' ¹¹⁻²⁰

Base Case Risk: What History Says About IPOs

Setting aside SpaceX’s specific financial profile, the historical evidence on Initial Public Offerings is worth examining directly.

Dimensional Fund Advisors studied more than 6,000 US IPOs from 1991 to 2018 and found that as a group they returned 6.93% annualized, compared to 9.13% for the broad market over the same period.⁸

In addition, the research found this underperformance is not random. It is explained by investment factor characteristics. IPOs as a group tend to exhibit:

Small companies

Growth oriented (i.e. high prices versus an accounting metric)

Low profitability, and

High-investment stocks (i.e. firms that grow assets aggressively)

These are precisely the characteristics that decades of academic evidence associate with lower expected future returns. Comparing SpaceX to these investment factors and the details in Figures 1 and 2, we see SpaceX is:

A large company

Extremely growth oriented (94x revenue multiple)

Extremely low profitability (negative profits as an entity)

Capital intensive, high-investment stock due to satellite, spaceship, data centres⁷

Key Risk Insight

While not perfectly predictive of the future, SpaceX exhibits some of the factors of companies that struggle to grow into their valuations.

Governance Risk: Live by the Musk, Die by the Musk

SpaceX is listing with a dual-class share structure: Class A shares (1 vote each, available to the public) versus Class B shares (10 votes each, held by Elon Musk). Post-IPO, Elon Musk controls 85% of the company's voting power.⁹ This is not unusual in technology IPOs. But the governance picture at SpaceX is materially more complex than a typical founder-controlled company. To highlight just a few of the governance abnormalities:

Musk simultaneously serves as CEO, CTO, and Chairman of SpaceX, while acting as CEO of Tesla, principal of the privately-held The Boring Company, and, prior to February 2026, controlling shareholder of xAI – which was merged into SpaceX.⁹

Tesla executives utilize SpaceX corporate aircraft for business travel under a formal related-party agreement, with SpaceX invoicing Tesla on a cost-reimbursement basis – totalling $4 million in cumulative flight charges from 2023 through 2025.¹

A Musk-owned security firm is paid by SpaceX for his personal security. These related-party relationships are disclosed in the S-1 as material.¹

Musk has pledged 237,530 Class A shares as collateral against personal loans.¹

The "Derivative Claim" Problem: Under a provision in Texas corporate law adopted by SpaceX's charter, a shareholder must own at least 3% of all outstanding shares – approximately $53 billion worth at the IPO expected $1.77 trillion valuation – just to bring legal claim against management on the company's behalf. This provision, combined with Musk's 85% voting control means there is no practical legal or governance mechanism through which public shareholders can hold leadership accountable.¹⁰

Key Risk Insight

Under the current voting share structure, purchasing SPCX is not a vote on SpaceX’s engineering or even the space or A.I. industries. It is an unconstrained bet on Musk’s judgment, capacity, and continued engagement, with little opportunity for shareholders to influence outcomes if Musk performs poorly.

Applying the North Road Framework

At North Road, we evaluate investment decisions through our Goals and Portfolio Strategy Report (GPS) framework, anchored to each client’s unique goals, time horizon, and capacity for risk.

The defining characteristic of the most dangerous portfolio situations we see is not asset class; it is concentration. Our approach is built on broadly diversified, factor-based investment funds, holding over 14,000 securities across asset classes and geographies, and with alternative strategies layered on where appropriate. The decision is never “should we own SpaceX?”. It is “which systematic factor exposures give our capital the highest probability of compounding over our desired time horizon?” Those are fundamentally different questions, and the difference is not incidental.

Thankfully, this approach allows us to participate in the breadth of global innovation and wealth creation without needing to predict if SpaceX (or any other company) will succeed on day one, nor predict if Elon Musk’s 85% voting shares will be a help or a hindrance.

So, while we will be watching the news on 2026’s new IPOs with anticipation, we will not put too much weight on these lottery tickets.

If you have questions about SpaceX or how any other investment fits within your overall plan: call us.

Sources

[1] SpaceX S-1 Registration Statement, SEC EDGAR, filed May 20, 2026. https://www.sec.gov/Archives/edgar/data/1181412/000162828026036936/spaceexplorationtechnologi.htm

[2] SpaceX S-1, SEC EDGAR: Space segment: $4.086B revenue, -$657M operating loss, 2025; >$15B cumulative Starship spend. https://www.sec.gov/Archives/edgar/data/1181412/000162828026036936/spaceexplorationtechnologi.htm

[3] SpaceX S-1, SEC EDGAR: Connectivity (Starlink) segment: $11.387B revenue, $4.423B operating income, 2025. https://www.sec.gov/Archives/edgar/data/1181412/000162828026036936/spaceexplorationtechnologi.htm

[4] TechCrunch, ‘xAI burned $6.4B last year’, May 20, 2026. https://techcrunch.com/2026/05/20/xai-burned-6-4b-last-year/

[5] Fortune, ‘SpaceX reveals its share price and record valuation: 555.6 million shares at $135 apiece, at a $1.77 trillion valuation’, June 3, 2026. https://fortune.com/2026/06/03/spacex-ipo-share-price-index-funds-valuation-public/

[6] Alphabet Inc., Annual Report 2025. Total revenues: $402.836 billion for the year ended December 31, 2025. SEC EDGAR filing. Calculation: $402.8B x 94x = $37.9 trillion implied valuation. For reference, Alphabet’s actual market capitalization as of June 2026 is approximately $2 trillion, implying a revenue multiple of roughly 5x. https://www.sec.gov/Archives/edgar/data/0001652044/000130817926000344/goog014907-ars.pdf.

[7] Morningstar, ‘6 Charts on SpaceX’s Pre-IPO Financials’, May 2026: Q1 2026 net loss $4.28B. https://www.morningstar.com/stocks/6-charts-spacexs-s-1-financials

[8] Dimensional Fund Advisors, ‘IPOs: Profiles Are High. What About Returns?’, August 2019. https://www.dimensional.com/gb-en/insights/ipos-profiles-are-high-what-about-returns

[9] SpaceX S-1, SEC EDGAR: Governance: dual-class structure, Musk 42% equity / 85.1% voting power. https://www.sec.gov/Archives/edgar/data/1181412/000162828026036936/spaceexplorationtechnologi.htm

[10] SpaceX Maps Texas Strategy to Dodge Securities Class Actions. Bloomberg Law. June 3, 2026. SpaceX Maps Texas Strategy to Dodge Securities Class Actions

[11] SpaceX S-1 Registration Statement. SEC EDGAR. Filed May 20, 2026. https://www.sec.gov/Archives/edgar/data/1181412/000162828026036936/spaceexplorationtechnologi.htm

[12] NVIDIA Corporation. Form 8-K — Fourth Quarter and Fiscal Year 2026 Results. SEC EDGAR. Filed February 25, 2026. https://www.sec.gov/Archives/edgar/data/0001045810/000104581026000019/q4fy26pr.htm

[13] Alphabet Inc. Form 8-K — Fourth Quarter and Fiscal Year 2025 Results. SEC EDGAR. Filed February 4, 2026. https://www.sec.gov/Archives/edgar/data/0001652044/000165204426000012/googexhibit991q42025.htm

[14] Microsoft Corporation. Form 8-K — Third Quarter Fiscal Year 2025 Results. SEC EDGAR. Filed April 30, 2025. https://www.sec.gov/Archives/edgar/data/0000789019/000095017025061032/msft-ex99_1.htm

[15] Microsoft Corporation. Form 8-K — Fourth Quarter and Fiscal Year 2025 Results. SEC EDGAR. Filed July 30, 2025. https://www.sec.gov/Archives/edgar/data/0000789019/000095017025100226/msft-ex99_1.htm

[16] Microsoft Corporation. Form 8-K — First Quarter Fiscal Year 2026 Results. SEC EDGAR. Filed October 29, 2025. https://www.sec.gov/Archives/edgar/data/0000789019/000119312525256310/msft-ex99_1.htm

[17] Microsoft Corporation. Form 8-K — Second Quarter Fiscal Year 2026 Results. SEC EDGAR. Filed January 29, 2026. https://www.sec.gov/Archives/edgar/data/0000789019/000119312526027198/msft-ex99_1.htm

[18] NVIDIA Corporation (NVDA). Historical Prices. Yahoo Finance. Closing price June 5, 2026: $205.10. https://finance.yahoo.com/quote/NVDA/history/

[19] Microsoft Corporation (MSFT). Historical Prices. Yahoo Finance. Closing price June 5, 2026: $416.67. https://finance.yahoo.com/quote/MSFT/history/

[20] Alphabet Inc. (GOOGL). Historical Prices. StockAnalysis.com. Closing price June 5, 2026: $368.53. https://stockanalysis.com/stocks/googl/history/

Disclaimer

This document is provided for informational purposes only and does not constitute investment, financial, legal, or cybersecurity advice. In our opinion, the information presented reflects common practices, general observations, and academic research; however, it may not be appropriate for all individuals or situations. The content is intended to support general understanding and awareness and should not be relied upon as a substitute for professional advice.

While we strive to offer effective guidance on digital safety, we cannot guarantee absolute protection against all online threats. The rapidly evolving nature of digital risks means that no measures can ensure complete security. As a result, it is not possible to provide guarantees of safety in connection with our Digital Risk Program. Any information or guidance given to address specific issues are based on best efforts and should not be construed to guarantee protection or to exhaustively address such issues.

Please note that any recommendations we provide are entirely optional, and you are under no obligation to act upon them. Should you choose to implement our suggestions, we may recommend you engage third-party service providers to implement some, or all, of the recommendations developed as part of Digital Risk Program. We do not receive compensation for referring these third-party providers, nor are you required to work with any third-party we recommend. Any engagement with a third-party provider is solely between you and the third-party. We recommend you perform your own due diligence on the expertise of third-party providers recommended by North Road. Any action taken by you or a third-party provider based on information, suggestions, or guidance provided by North Road under the Digital Risk Program is entirely the responsibility of the acting party and North Road does not take any responsibility or ownership of any such action.

All opinions, projections and estimates herein reflect the author's judgment as of the date of the document, may not be realized, and are subject to change without notice. Nothing in this document is or should be relied upon as a promise or representation as to the future.

©2026 North Road Investment Counsel Inc. All rights reserved.